Quick Summary: Flexible Dues & Micro-Memberships

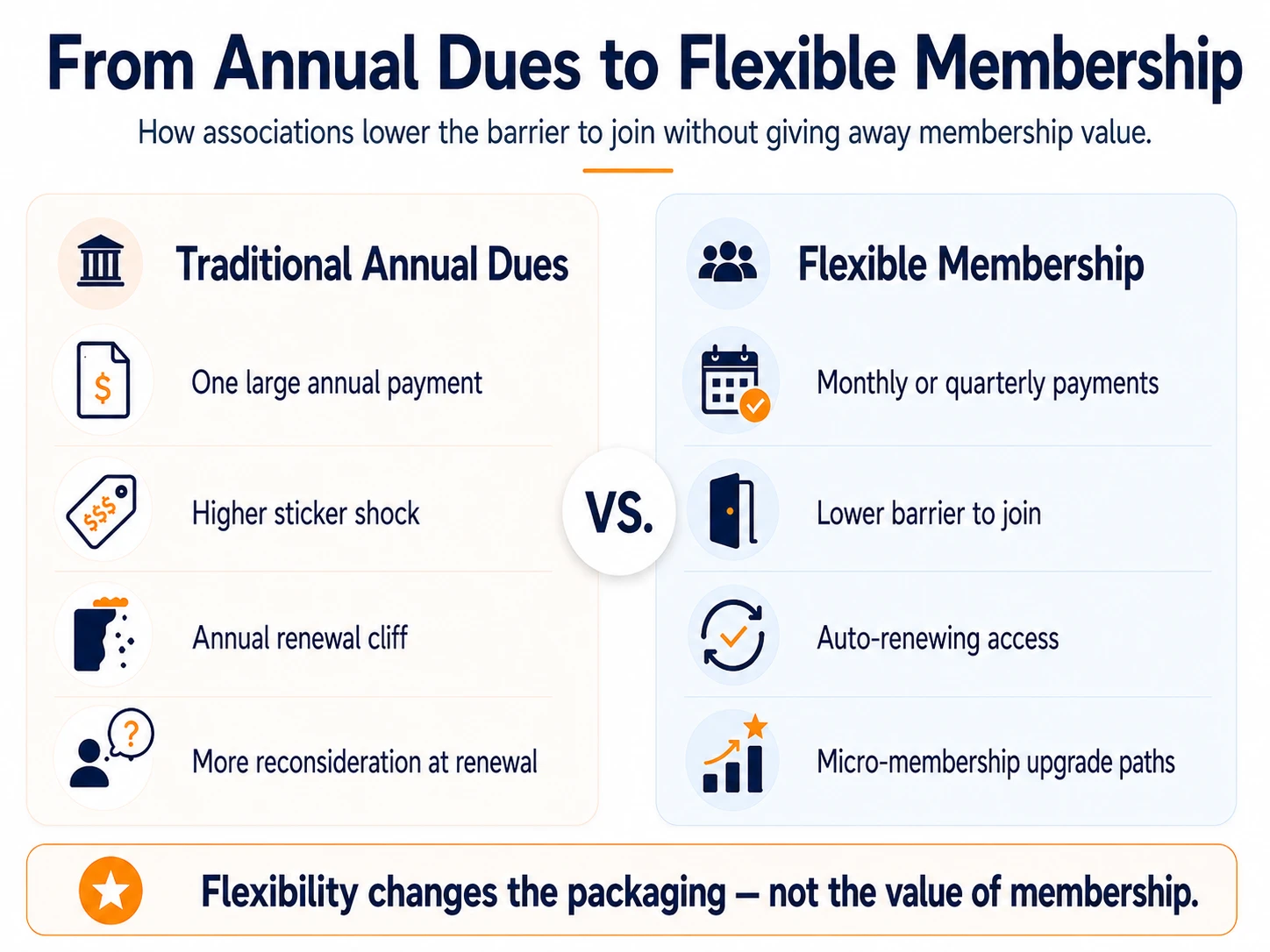

- The annual-dues model is straining, not dead. Younger professionals balk at one big up-front payment—so the fix is flexibility, not abandoning dues.

- Flexible dues lower the barrier to join: monthly, quarterly, and installment billing spread the cost and reduce sticker shock at renewal.

- Micro-memberships create on-ramps: event-only or community-only access at a low price point turns hesitant prospects into members you can upgrade later.

- The trade-off is revenue predictability—offset it with auto-renewing billing, failed-payment recovery, and annual-pay incentives.

- It only works if your AMS can handle it: installments, prorations, and failed-payment recovery have to be automated, or flexibility becomes a manual headache.

For decades, the association membership model was simple: one annual fee, paid up front, renewed once a year. It worked because that's how professional membership had always worked.

And it really has always worked that way—for longer than you might think. The word "guild"—the medieval ancestor of today's professional association—traces back to a root meaning "to pay." Membership and dues have been intertwined for the better part of a thousand years. What's changing in 2026 isn't whether members pay. It's how.

The annual model is now under real strain. In late 2025, ASAE argued that the traditional membership model is breaking down—not because membership has lost its value, but because the way associations package and price it no longer matches how younger professionals expect to buy. Raised on monthly subscriptions, early-career members increasingly hesitate at a single large up-front payment, even when they value what's on the other side of it.

The answer isn't to abandon dues. It's to make them flexible. Flexible dues and micro-memberships are how associations lower the barrier to join, reach younger members, and reduce the sticker shock that drives renewal-time churn—without giving away the value of membership.

This guide covers the practical models, the real trade-offs, and what it actually takes to run flexible billing without drowning your staff in manual work.

Why the annual-dues model is straining

A few forces are converging:

- Generational expectations. Younger professionals are used to paying for everything—software, media, gyms—in small monthly increments. A $400 annual ask feels heavier to them than to the members who've always paid it.

- The "membership cliff." Many associations face an aging core membership and slower replacement from younger cohorts. Rigid pricing makes that gap harder to close.

- Value-sensitivity. Early-career professionals question the ROI of membership when they can find free content online. A lower-commitment entry point lets them try before they fully buy in.

This isn't an association-specific quirk—it's the whole economy. Subscription-based businesses have grown revenue faster than the S&P 500 over the past decade, and 68% of consumers signed up for a new subscription service for the first time in 2024. Your members live in that world all day; a once-a-year, pay-it-all-now ask increasingly feels out of step with it.

None of this means dues are obsolete. It means the packaging needs to flex. For the broader picture, see our guide to membership pricing strategies.

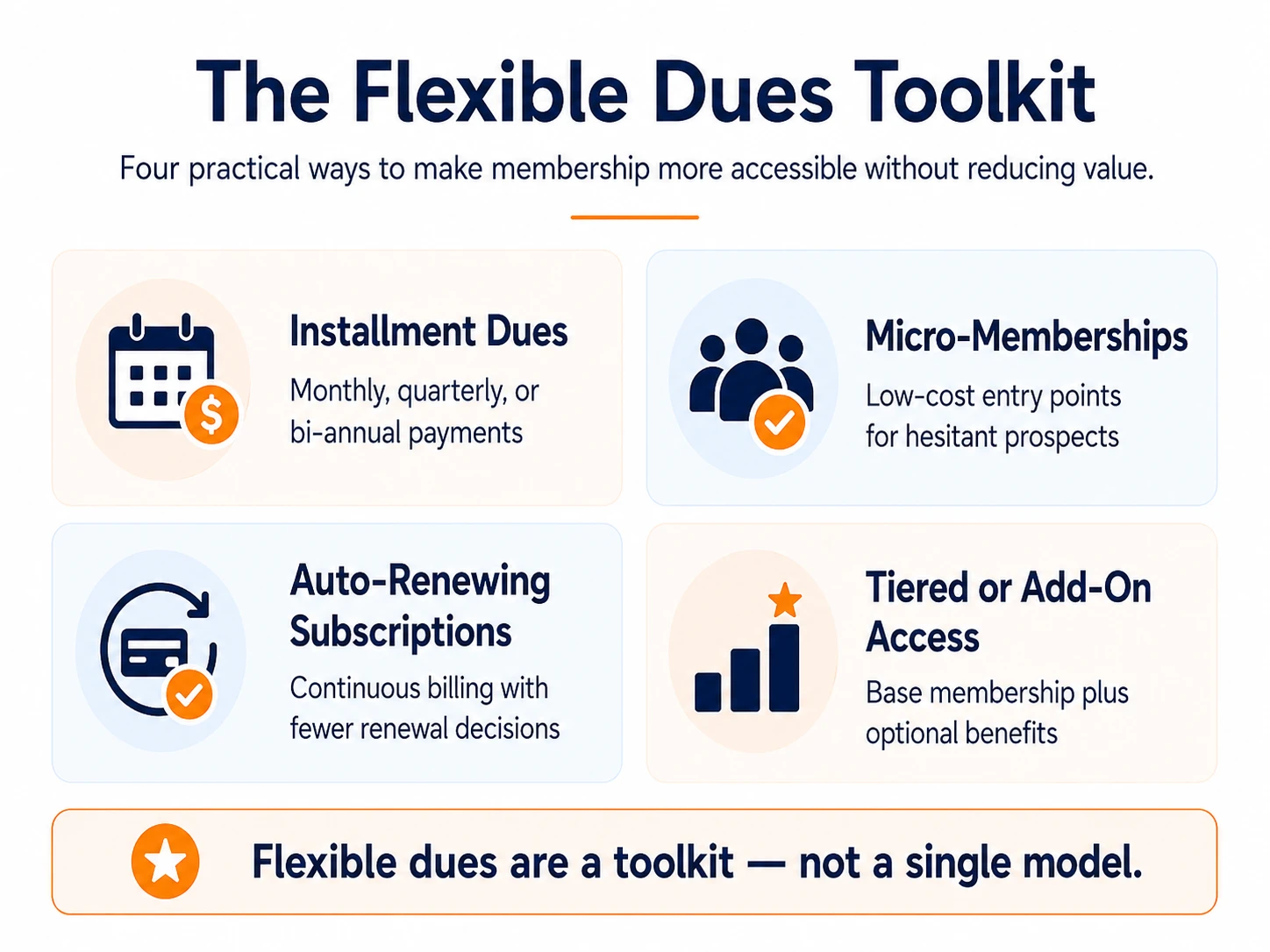

The flexible-dues toolkit

Here are the models associations are using in 2026, from simplest to most involved.

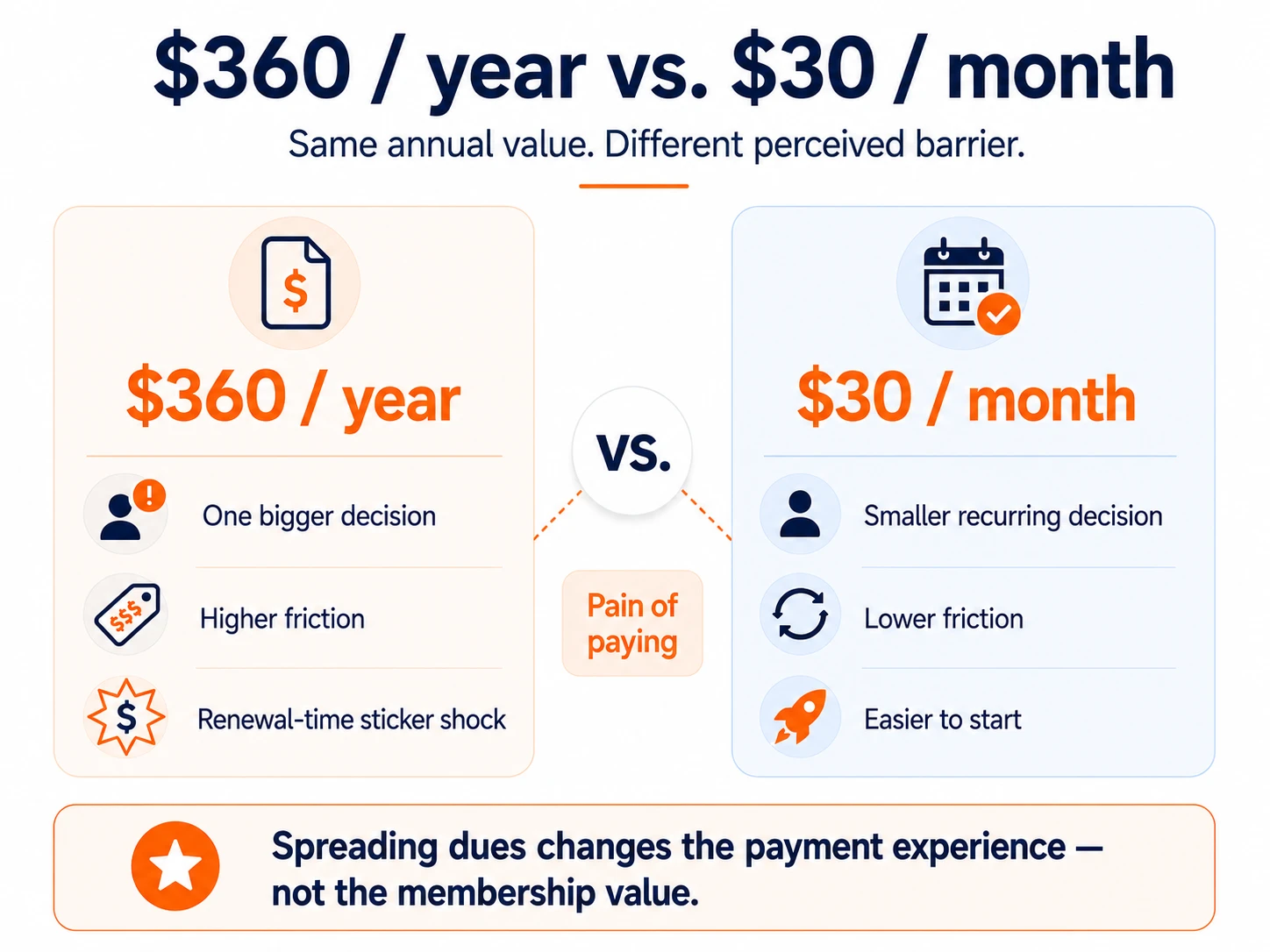

1. Installment dues (monthly, quarterly, bi-annual)

The simplest change: keep your annual price, but let members spread it across smaller payments. A $360 annual dues becomes $30/month or $90/quarter.

- Lowers the barrier to join—$30 feels far more approachable than $360.

- Reduces silent churn. Smaller, automated payments avoid the once-a-year moment where a member reconsiders the whole expense.

- Keeps you top-of-mind. A monthly touchpoint reinforces value all year, not just at renewal.

The behavioral science behind it: There's a real reason $30/month feels easier than $360/year. Economists call it the "pain of paying." Research by Prelec and Loewenstein found that decoupling the purchase from the payment—exactly what a monthly charge or subscription does—measurably reduces that pain and raises what people are willing to pay. Spreading dues across the year isn't a discount; it's a smaller, less painful decision, repeated.

2. Micro-memberships

A micro-membership is a low-priced, limited tier—event-only access, community-only access, or a digital-resources pass—that gives prospects an affordable on-ramp.

- It converts "not sure it's worth it" prospects into paying members.

- It creates a natural upgrade path to full membership once they've experienced the value.

- It captures revenue from people who would otherwise never join at full price.

3. Auto-renewing subscriptions

Treat dues like any modern subscription: continuous, low-friction, and easy to start. Auto-renew with a stored payment method is the single biggest lever for retention—it removes the active decision to re-up every year. More in our guide to automating membership renewals.

4. Pay-for-what-you-use and tiered access

Some associations let members assemble their own membership—a base rate plus optional add-ons (events, certifications, premium content). It's more complex to run, but it lets price-sensitive members start small and grow their spend over time.

The benefits, plainly

- A wider front door. Lower entry points bring in members who would have said no to the full annual price.

- Less renewal-time churn. Spreading the cost removes the annual sticker-shock moment that triggers non-renewals—one of the biggest, most preventable sources of churn. See reducing membership churn.

- Younger members. Flexible billing matches how early-career professionals expect to pay, widening your pipeline against the membership cliff. See young professional engagement.

- Steadier cash flow. Monthly billing produces predictable recurring revenue across the year instead of one annual spike.

The honest trade-offs

A practical guide has to name the downsides:

- Revenue is harder to forecast. Members on monthly plans can cancel anytime, so you can't bank a full year of dues up front.

- More moving parts. Prorations, mid-cycle upgrades, and failed payments multiply the billing scenarios your team has to handle.

- Potential for lower lifetime value if members who would have paid annually downgrade to month-to-month and churn sooner.

How associations offset these:

- Auto-renewing billing and failed-payment recovery keep monthly revenue from leaking out through expired cards and forgotten invoices.

- Annual-pay incentives—a small discount for paying yearly—nudge members who can toward the more predictable option.

- A real grace period prevents accidental lapses from failed payments. See grace period best practices.

How to roll it out

You don't have to overhaul everything at once:

- Start with installments on your existing dues. Offer monthly or quarterly as an option alongside annual. Low risk, immediate accessibility win.

- Add one micro-membership on-ramp. Pick your most popular benefit—events or community—and offer a low-priced, limited tier around it.

- Default new members to auto-renew. Make continuous billing the standard, with clear notice before each charge.

- Automate the billing cycle. Installments, prorations, and failed-payment retries should run without staff touching them.

- Measure and adjust. Track join rate, retention by payment type, and lifetime value. Keep what grows the base without eroding value.

It lives or dies in your AMS

Here's the part that determines whether flexible dues are a growth lever or a staff headache: flexible billing only works if your association management software can handle installments, prorations, automatic renewals, and failed-payment recovery cleanly.

Run it on a platform that can't, and every month becomes a manual reconciliation exercise—exactly the busywork flexible pricing was supposed to avoid. Run it on one that can, and the same flexibility that attracts members runs quietly in the background. The strategy is sound; the operational details are where it succeeds or fails. This is also why your payment setup matters—see payment processing best practices.

The bottom line

The associations winning the next generation of members aren't lowering their value—they're lowering the barrier to access it. Flexible dues and micro-memberships meet younger professionals where they are, reduce renewal-time churn, and widen the front door, as long as the billing runs on automation instead of staff time. Start with installments, add one micro-membership on-ramp, default to auto-renew, and let your AMS do the heavy lifting.

Key takeaways

- Make dues flexible, don't abandon them: the model is straining because of packaging, not value.

- Installments lower the barrier: $30/month feels far easier than $360/year—and behavioral science backs that up.

- Micro-memberships are on-ramps: low-price, limited tiers convert hesitant prospects you can upgrade later.

- Offset the revenue trade-off: auto-renew, failed-payment recovery, and annual-pay incentives keep cash flow steady.

- Automate it: flexible billing only works if your AMS handles installments, prorations, and recovery.

Frequently asked questions

What are flexible membership dues?

Flexible membership dues let members pay in smaller, more frequent installments—monthly, quarterly, or bi-annually—instead of one large annual payment. They lower the barrier to join and reduce churn caused by sticker shock at renewal.

What is a micro-membership?

A micro-membership is a low-priced, limited membership—such as event-only or community-only access—that gives prospects an affordable on-ramp to full membership and a natural path to upgrade later.

Do flexible dues hurt revenue predictability?

They can, because members on monthly plans can cancel anytime. Associations offset this with auto-renewing billing, failed-payment recovery, and annual-pay incentives, which keep recurring revenue steady.

Why are associations moving to flexible dues in 2026?

Younger professionals, shaped by subscriptions, increasingly hesitate at a single up-front annual payment. Flexible dues meet that expectation and widen the pool of people who will join.

What does an association need to offer flexible dues?

An association needs an AMS that can handle installment billing, prorations, automatic renewals, and failed-payment recovery. Without that automation, flexible billing creates more manual work than it is worth.

Ready to Offer Flexible Dues Without the Manual Work?

Monthly billing, installments, micro-memberships, and auto-renewals only work when the billing runs itself. i4a handles flexible dues, prorations, automatic renewals, and failed-payment recovery—so you can meet members where they are without adding work for your team.

See How i4a Handles Flexible DuesRelated resources

Tiered vs. flat pricing, and how flexible dues fit into your broader pricing model.

How to Reduce Membership Churn

Why renewal-time sticker shock drives churn—and how to design it out.

Auto-renew and failed-payment recovery—the engine behind flexible billing.

Young Professional Member Engagement

Reaching the early-career members flexible dues are designed to attract.